COMMERCIAL COLLECTION FIRM OF AMERICA

Introduction: The Race Against Time

Every business that extends credit will eventually face the same problem: a customer that doesn't pay. Whether you're a business owner watching receivables age past 90 days, an accounts receivable manager juggling dozens of past-due accounts, or a CFO trying to protect cash flow, the question is the same - how do you collect an unpaid business debt without burning time, money, and the client relationship in the process?

This guide walks you through the full commercial collection process - internal efforts, demand letters, collection calls, payment plans, agency placement, asset investigation, and litigation - with the data behind each decision point, so you know exactly what to do at each stage and when it's time to escalate.

The Cost of Waiting: What the Data Shows

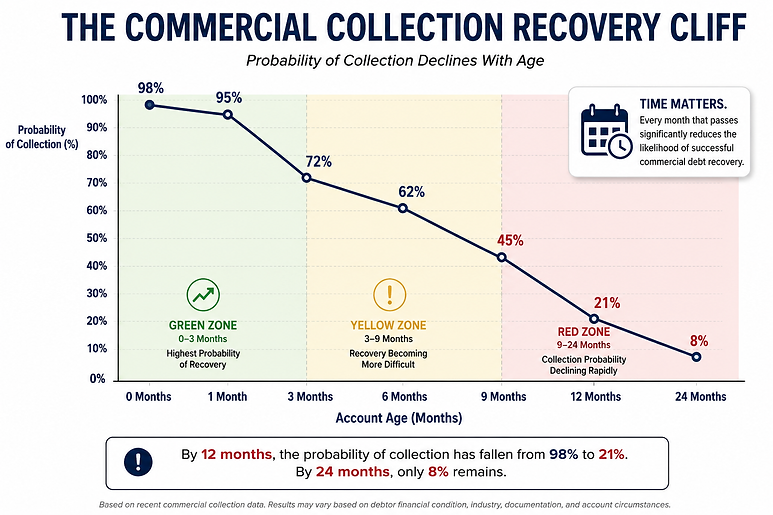

Before walking through the process, it's worth understanding why the process has deadlines. Aged debts are harder to collect for predictable reasons: debtor businesses close, assets get moved or pledged to faster-moving creditors, documentation goes stale, and contacts disappear. The decline isn't gradual - it accelerates.

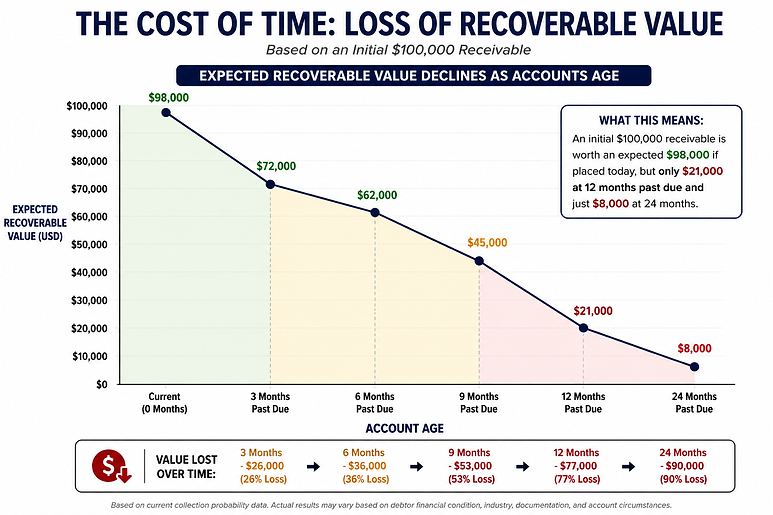

Translate those percentages into dollars and the urgency becomes concrete. A $100,000 receivable is worth roughly $72,000 in expected value at three months past due, and roughly $21,000 at twelve months. Every quarter an account sits unworked, real money evaporates from your balance sheet.

THE RULE THIS DATA SUPPORTS: Set a hard internal escalation deadline - typically 90 to 120 days past due - and honor it without exception. The 90-180 day window is where third-party intervention preserves the most value.

You're Not Alone: The Scale of the Problem

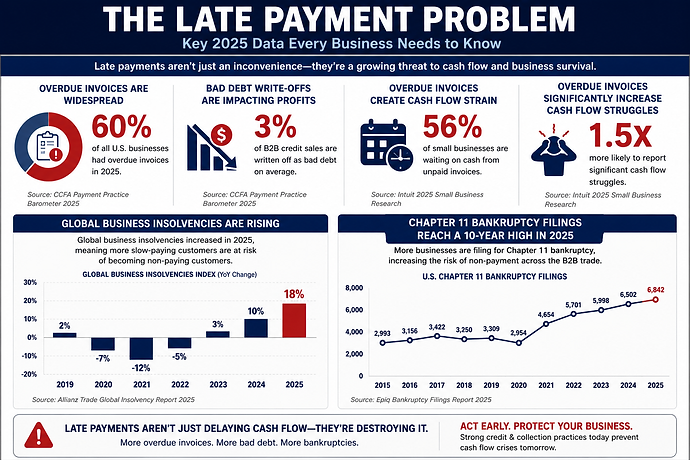

Late payments have become a serious financial threat in B2B trade. In 2025, many U.S. businesses experienced overdue invoices, with bad debt write-offs cutting into revenue and unpaid invoices creating major cash flow strain. The data also shows that businesses heavily affected by overdue invoices are far more likely to struggle with cash flow, while rising insolvencies and Chapter 11 bankruptcy filings increase the risk that slow-paying customers may eventually become non-paying customers.

The takeaway for credit managers is clear: the cost of waiting is increasing. In today’s environment, overdue invoices are no longer just a temporary cash flow issue. They are becoming a direct indicator of credit risk. With 60% of businesses reporting overdue invoices, rising business insolvencies, and Chapter 11 filings reaching a 10-year high, credit managers cannot assume that a slow-paying customer will eventually pay. The longer an account remains unpaid, the greater the likelihood that the debtor’s financial condition will deteriorate, reducing the probability of recovery altogether.

As a result, credit managers should identify delinquent accounts earlier, enforce credit terms consistently, reduce collection delays, and escalate high-risk accounts before they become uncollectible. In an economy where financial distress is rising, proactive credit and collection management is no longer just about improving cash flow. It is about protecting receivables before they turn into bad debt.

Bottom Line: Every overdue invoice should be viewed as both a collection issue and a potential credit risk. The sooner action is taken, the greater the likelihood of preserving the value of the receivable.

Before You Begin: Confirm the Debt is Collectible

In business-to-business collections, the strength of your paper trail determines the strength of your position. Before you send a single demand or pick up the phone, assemble:

-

The contract, credit application, or purchase order establishing the obligation

-

Signed delivery confirmations, work orders, or acceptance records proving you performed

-

All invoices and statements showing amounts, dates, and terms

-

Email and correspondence history, including any acknowledgment of the debt or promises to pay

-

Personal guarantees, if any were signed - these dramatically improve your leverage

Verify the basics, too: Is the legal entity name on your invoice correct? Is the business still operating? Has it changed names, merged, or filed for bankruptcy? Collecting from the wrong entity - or chasing a dissolved one - wastes everyone's time.

Finally, identify disputes early. A debtor who claims your product was defective or your service incomplete is a different problem from a debtor who simply won't pay. Disputed debts require documentation and negotiation strategy; undisputed debts require pressure and persistence. Know which one you're dealing with before you start.

Step 1: Internal Collection Efforts (Days 1-30)

Most overdue payments from clients aren't acts of defiance - they're the result of cash flow timing, lost invoices, internal approval bottlenecks, or simple disorganization. Atradius found the leading cause of U.S. B2B late payment was administrative inefficiency in customers' payment processes, and that overdue invoices were converted to cash an average of 20 days past due. Your first moves should assume good faith while establishing a clear record.

Send a friendly payment reminder immediately. The day an invoice goes past due, send a short, professional reminder with the invoice attached. Many payments shake loose at this stage with no friction at all.

Follow up by phone within a week. Email is easy to ignore; a call is not. Confirm receipt, confirm there's no dispute, and ask directly: "When can we expect payment?" Get a date, then confirm it in writing.

Document everything. Every call, email, and promise to pay - date, contact, and what was said. This record becomes critical evidence if the matter escalates, and prevents the debtor from claiming they were never contacted.

Stop extending credit. Put new orders on hold for seriously past-due accounts. Continuing to supply a non-paying customer deepens the loss - and the credit hold itself is often your strongest leverage.

Step 2: Escalate Internally (Days 30-60)

If friendly reminders haven't worked, change the tone and the messenger.

Move the conversation up the chain. Have a controller, credit manager, or owner contact their counterpart at the debtor company. Peer-to-peer contact between decision-makers often breaks logjams that AP clerks can't - or won't - resolve.

Send a firm past-due notice. State the amount owed, reference invoices and contract terms, note any late fees or interest your agreement allows, and set a specific payment deadline.

Diagnose the real situation. Is this a can't pay problem (cash flow trouble, seasonal crunch) or a won't pay problem (dispute, dissatisfaction, or strategic stalling)?

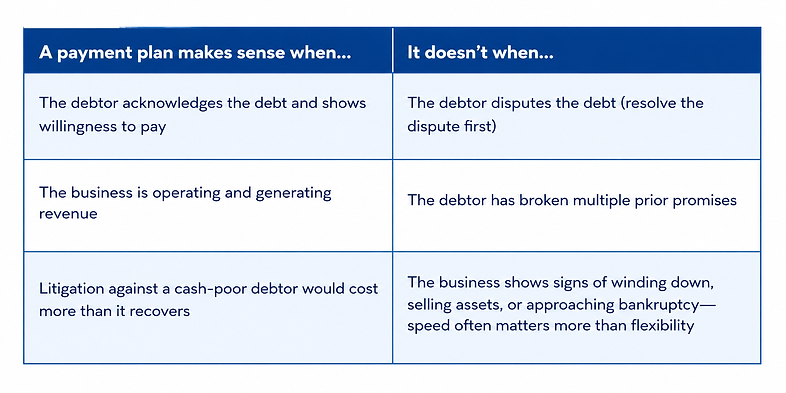

The answer determines your next move. Can't pay points toward a structured payment plan before the situation deteriorates. Won't pay with a dispute means getting the dispute in writing, evaluating it honestly, and rebutting it with documentation. Won't pay, no reason given - silence and broken promises - is the clearest signal that voluntary collection is failing and escalation should accelerate.

Step 3: The Formal Demand Letter (Days 60-90)

The demand letter is the pivot point of the entire collection process - the moment your effort shifts from customer service to debt recovery. Done correctly, a final demand resolves a substantial share of commercial debts without further escalation.

An Effective demand letters includes:

-

A precise statement of the debt - total amount due, invoice numbers, dates, and any contractual interest or late fees

-

The basis for the obligation - reference to the contract, credit agreement, or purchase orders

-

A firm deadline - typically 7 to 10 business days, stated as a specific calendar date

-

The consequence of non-payment - referral to a commercial collection agency or legal counsel, which may affect the debtor's business credit standing

-

Clear payment instructions - exactly how and where to pay

What to avoid: threats you won't follow through on, abusive language, and vague deadlines like "immediately." Idle threats destroy credibility - if you say the account goes to collections in 10 days, it must actually go to collections in 10 days. Debtors learn quickly which creditors bluff.

Delivery matters. Send the final demand by certified mail with return receipt (or another trackable method) and by email, so you have proof of receipt. And note: a demand letter on a collection agency's or attorney's letterhead carries substantially more weight than one on your own. Debtors understand that once a third party is involved, the cost of ignoring the debt just went up - many pay at this exact moment for that exact reason.

Step 4: Collection Calls That Actually Work

Phone calls remain the single most effective tool in commercial collections - but only when handled with preparation and discipline.

Before the call:

-

Know the full account history: amounts, dates, prior promises, and any disputes

-

Identify the right contact - ideally the owner, CFO, or controller, not a gatekeeper

-

Decide in advance what you'll accept: payment in full, a settlement floor, or payment plan terms

An agency's answers to these questions will tell you whether they're the cream of the crop or just another volume player.

During the call:

State the purpose immediately. "I'm calling about the $42,500 balance that is now 75 days past due."

Then stop talking. Silence is uncomfortable, and debtors fill it - often with information you need: their cash position, their disputes, their intentions.

Ask open questions. "What's preventing payment?" surfaces the real obstacle faster than accusations do.

Counter excuses with specifics. "The check is in the mail" → "What's the check number and the date it was mailed?"

Close with a commitment. Every call ends with a specific promise - amount, date, method - confirmed in writing within the hour.

After the call: if the promised payment date passes without payment, call the same day. Letting broken promises slide teaches the debtor that your deadlines are negotiable.

Step 5: Payments Plans: When and How to Use Them

A structured payment plan is often the difference between recovering most of a debt and recovering none of it. When a debtor genuinely can't pay in full but the business is viable, an installment arrangement keeps money flowing to you instead of to faster-moving creditors.

Structure the plan to protect yourself

-

Get it in writing - always. A signed agreement stating the total owed, the installment schedule, and where payments go.

-

Include an acknowledgment of the debt. The debtor's written admission eliminates dispute defenses later and can reset the statute of limitations clock.

-

Add an acceleration clause. One missed payment makes the entire remaining balance immediately due.

-

Get a down payment. A meaningful first payment - ideally 20-30% - proves commitment and reduces exposure immediately.

-

Consider security. A personal guarantee, confession of judgment (where enforceable), or security interest in assets transforms an IOU into real protection.

-

Keep the term short. Three to six months is reasonable for most commercial debts. A 24-month plan on a $30,000 debt is a slow-motion write-off.

MONITOR CLOSELY: The first missed payment is your signal. Invoke the acceleration clause and escalate immediately - debtors who default on payment plans rarely cure on their own

Step 6: Engaging a Commercial Collections Agency (Day 90+)

When internal efforts stall - broken promises, ignored demands, calls that go to voicemail - it's time to stop doing this yourself. This is the point where many businesses lose the most money, not by acting, but by waiting. Recall Figure 1: the difference between placing an account at 90 days and placing it at 300 days is routinely the difference between recovery and write-off.

Why a commercial collections agency changes the dynamic:

-

Third-party pressure is psychologically different. A demand from a collection firm signals the creditor is serious, the debt may reach commercial credit bureaus, and litigation is the next stop. Debtors who ignored you for months frequently engage within days.

-

Specialization matters. Commercial (B2B) collections is a different discipline from consumer collections - corporate structures, officer liability, contract disputes, and business-to-business negotiation dynamics.

-

Contingency pricing aligns incentives. Most reputable commercial agencies are paid a percentage of what they actually recover - and nothing if they recover nothing. Escalation carries no additional out-of-pocket cost.

-

Your team gets back to its real job. Every hour AR staff spends chasing a 120-day-old debt is an hour not spent managing current receivables - where delinquencies are prevented in the first place.

What to expect when you place an account:

A competent commercial collections agency moves fast - written demand within a day, phone contact shortly after, and a candid early assessment of collectibility. Within 30-60 days you should know whether the account will resolve voluntarily, needs a negotiated settlement, or requires investigation and legal escalation.

Step 7: Asset & Liablity Investigation: Know Before You Sue

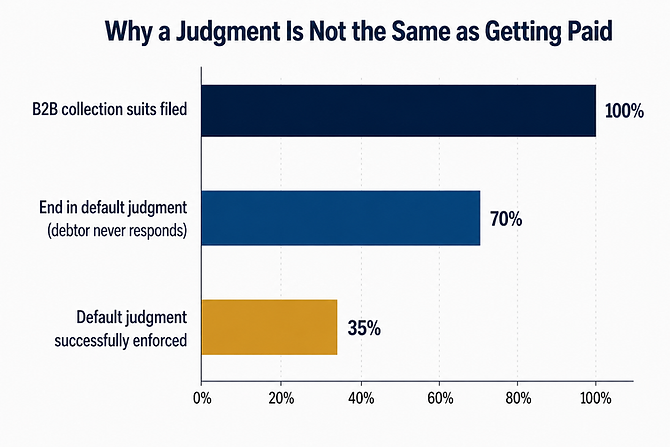

Here's the question too few creditors ask before filing suit: even if I win, can I collect? A judgment is not money. It's a court's confirmation that you're owed money - and against a debtor with no reachable assets, it's an expensive piece of paper. Industry analysis indicates more than 70% of B2B debt lawsuits end in default judgment, but only about half of those judgments are ever successfully enforced.

A proper pre-suit investigation examines:

-

Business status and structure - active, in good standing, or quietly dissolved? Related entities, successor companies, or "phoenixing" patterns?

-

Real property and equipment owned by the business or its principals that could satisfy a judgment

-

Banking relationships - identifiable accounts subject to garnishment or levy after judgment

-

Receivables and revenue streams - ongoing contracts and customer payments that could be intercepted post-judgment

-

Liens, judgments, and UCC filings - if secured creditors, tax liens, and prior judgments are stacked up, you may be at the back of a long line

-

Litigation and bankruptcy history - a debtor with a bankruptcy filing on the horizon changes the calculus entirely.

Skip-tracing matters too when debtors go dark: locating principals who've moved, identifying current operating addresses, and finding the decision-maker hiding behind a disconnected phone number. The output of this work is a clear-eyed recommendation: this debtor has reachable assets and litigation is justified, or this debtor is judgment-proof and your money is better spent elsewhere. Either answer is valuable. Suing a judgment-proof debtor doesn't recover bad debt - it compounds it with legal fees.

Step 8: Litigation and Post-Judgment Enforcement

When demands fail, negotiations collapse, and the asset investigation confirms the debtor can pay but won't, litigation is the remaining path.

The suit-worthiness decision. Litigation makes sense when three things align: the debt is well-documented, the amount justifies legal costs, and the debtor has reachable assets. Many commercial collection agencies maintain attorney networks and place suit-worthy accounts with counsel in the debtor's jurisdiction - often on contingency or blended-fee terms that keep your downside controlled.

Filing and the settlement window. A surprising number of commercial cases settle shortly after the complaint is served. Being sued is expensive for the debtor too, and the prospect of a public judgment damaging their credit and reputation is often the leverage that finally produces a check.

Default or judgment. Many commercial debtors never respond to the complaint, resulting in default judgment. Contested cases proceed through discovery toward trial, though most resolve by settlement along the way.

Post-judgment enforcement - where the asset investigation pays off:

-

Bank levies - seizing funds directly from identified accounts

-

Garnishment of receivables - intercepting payments owed to the debtor by its customers

-

Liens on real property - clouding title until the debt is paid

-

Seizure and sale of business assets - equipment, inventory, vehicles

-

Debtor examinations - court-ordered testimony under oath about assets and income

A NOTE ON TIMING:

Every state imposes a statute of limitations on contract claims - commonly three to six years, varying by state and claim type. Waiting too long doesn't just reduce collectibility; it can extinguish your legal rights entirely. If a debt is aging, the clock is running.

Final Thoughts

Collecting an unpaid business debt isn't about aggression - it's about process, persistence, and knowing when to escalate. Most commercial debts are recoverable when worked promptly and systematically: clear documentation, firm demands, disciplined follow-up, smart use of payment plans, and timely escalation to professionals when internal efforts stall.

The data in this guide points to a single operating principle: the receivable on your books today is worth more than it will ever be again. Build your escalation timeline, follow it, and act inside the 90-180 day window where recovery odds are still on your side.

CARRYING UNPAID INVOICES?

A contingency-based commercial collection firm can evaluate your accounts at no upfront cost - you pay only when they recover. Commercial Collection Firm of America (CCFA) specializes in B2B debt recovery, from pre-litigation demand and negotiated resolution through asset investigation and attorney placement.

FREQUENTLY ASKED QUESTION'S

RECENT ARTICLES & INSIGHTS

LEARN MORE

>

>

>

>

COMPANY

>

>

>

>

Careers

SUPPORT

>

>

>

>

RESOURCES

>

>

>

Subscribe

>

Corporate Headquarters

Commercial Collection Firm of America

Address: 6105 S Main St. Suite 200

Aurora, CO 80016

Email: help@trustccfa.com

Tel: 1-888-799-3649

Fax: 1-888-351-2776

Hours: Monday - Friday, 7am -4pm (MST)

Explore our other locations by clicking here.